Listen to this article

"Using Gift Funds for a Home Purchase"

Gift Funds for a Home Purchase: What You Need To Know

Buying a home is expensive, and many borrowers rely on gift funds – money given by a family member or other approved donor – to help cover the down payment or closing costs. However, each loan program (Conventional, FHA, VA, USDA, Jumbo) has specific rules on who can give a gift, how it must be documented, and what pitfalls to avoid.

Below we break down the latest guidelines for gift funds by loan type, explain donor and documentation requirements, and highlight common missteps to help you navigate this process confidently.

What Are Gift Funds and Why Are They Important?

Gift funds are money given to the buyer with no expectation of repayment. That “no repayment” part is the key. If it is a loan, even a friendly one, it has to be treated differently in underwriting.

Most mortgage guidelines require:

- An eligible donor (depending on loan type)

- A signed gift letter

- A paper trail showing where the funds came from and where they went

In other words, gift funds are allowed, but they have to be documented like everything else in a mortgage.

Let's Talk About Your Goals

Have questions about this topic? Jon Dao is here to help you understand your options and guide you through the process.

What Gift Funds Can Cover

In most cases, gift funds can be used for:

- Down payment

- Closing costs (lender fees, title, escrow, etc.)

- Prepaid items (homeowners insurance, prepaid interest, property taxes, etc.)

- Discount points (if the buyer chooses to pay points)

Reserves are program dependent:

Conventional often allows gifts to help with reserves (subject to scenario).

VA and USDA generally do not allow gifts to satisfy reserve requirements in scenarios where reserves are required.

What You Need To Verify

1) A signed gift letter. At minimum, the gift letter should include:

- Gift amount (actual amount, or a maximum amount, depending on program/lender)

- Donor’s name, address, phone

- Relationship to the borrower

- Statement that no repayment is expected

- Signatures (donor, and often borrower)

2) Proof the donor had the funds and the funds were transferred

Common acceptable documentation (varies by program and how the gift is delivered):

- Donor check + borrower deposit slip

- Evidence of electronic transfer (wire or ACH) to borrower or to closing agent

- Donor check to closing agent + settlement/closing disclosure showing receipt

3) No cash deposits

Avoid cash in envelopes or cash deposits labeled as “gift.” Cash is difficult to source and commonly not acceptable as a gift source.

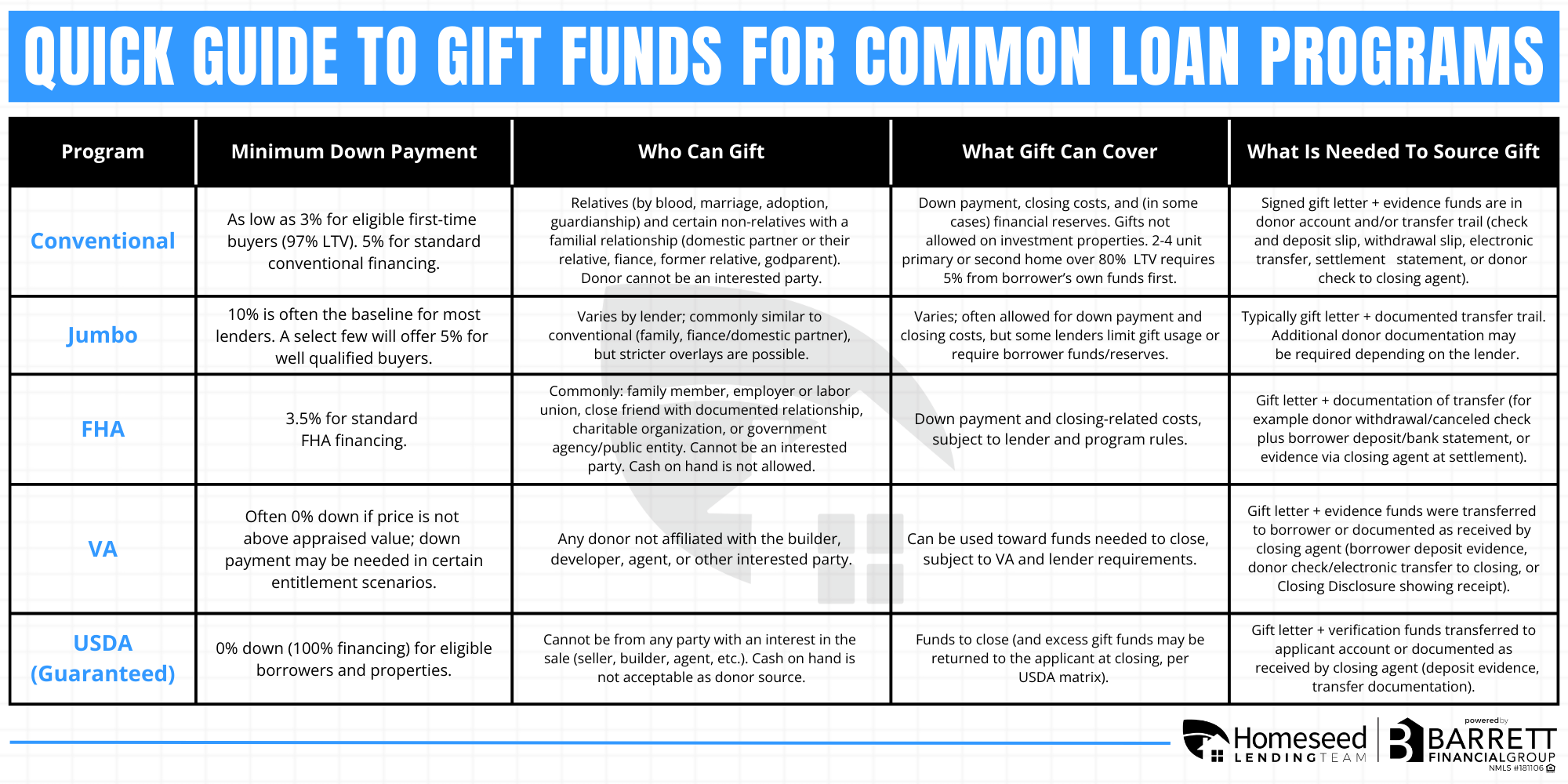

Quick Guide for Popular Loan Programs

Conventional (Fannie Mae and Freddie Mac)

Best for: Primary and second homes (not investment properties for agency conventional gift rules).

Highlights:

- Gifts can be used for down payment, closing costs, and (in many cases) reserves.

- No borrower contribution is required for: 1-unit primary (even when LTV > 80%) or Any primary/second home when LTV ≤ 80%

- Borrower must contribute 5% from their own funds when: 2–4 unit primary with LTV > 80%, or Second home with LTV > 80%

- Donor restrictions: donor cannot be affiliated with builder/developer/agent/other interested party.

- If donor has lived with borrower for 12 months (and will continue) there are special rules where the gift may be treated as the borrower’s own funds in certain cases.

Documentation you should expect:

- Gift letter

- Paper trail showing donor funds were available and transferred (or received by closing agent)

Jumbo and Non-QM

These vary by lender/investor and are not governed by a single national rule set.

Common patterns:

- Gifts often allowed from close relatives, sometimes broader

- Strong preference for gifts to be seasoned or clearly sourced

- Many programs require a minimum amount of borrower’s own funds or stronger reserve requirements

If you are using a jumbo/non-QM product, confirm gift rules before any transfers are initiated.

FHA

FHA is generally gift-friendly, but documentation matters.

Who can gift (common national categories):

- Family members (as defined by FHA policy)

- Employer or labor union

- Close friend with a clearly documented interest

- Charitable organization

- Government agency or public entity with homeownership assistance

Key rules:

- Gift letter is required and must include donor/borrower details and a statement that no repayment is required.

- Gift funds cannot be from “cash on hand” or cash saved at home.

- If the gift is coming from someone with an interest in the sale, it may be treated as an inducement to purchase rather than an eligible gift.

Gift of equity (FHA):

- Equity credit as a gift is permitted only in specific family-to-family scenarios and requires additional documentation.

VA

VA loans are typically 0% down, so gifts are commonly used for:

- Funds needed to close (closing costs, prepaids)

- Optional down payment to reduce loan amount

- Appraisal gap scenarios (case-by-case; structure early)

Key rules:

- Gift donor must not be affiliated with builder, developer, real estate agent, or any other interested party.

- Gift letter required (amount, no repayment statement, donor contact info, relationship).

- Lender must verify funds were transferred to borrower or documented as received by the closing agent.

- Gift funds cannot be used to meet reserve requirements when reserves are required (common in rental-income qualifying scenarios).

USDA (Guaranteed Rural Housing)

USDA is also typically 0% down, so gifts are often used for:

- Closing costs/prepaids

- Voluntary down payment (optional)

- Guarantee fee (if applicable in the transaction structure)

Key rules:

- Interested parties are not eligible gift donors.

- Gift funds may be provided directly to the title company with proper documentation.

- Gift funds are considered the applicant’s own funds, and in some cases excess gift funds may be eligible to be returned to the applicant at closing.

- Gift funds are not included in reserve calculations.

*This chart is a high-level overview for general educational purposes only and is not a commitment to lend. Gift fund eligibility, acceptable donors, documentation requirements, and minimum down payment rules vary by loan program, lender or investor overlays, property type, occupancy, and borrower qualifications, and guidelines can change. Confirm current requirements with your licensed mortgage professional before transferring funds.

Common Mistakes With Gift Funds

Waiting until the last week to move gift money

- Depositing cash instead of using a traceable transfer method

- Using an ineligible donor or an interested party

- Gift letter amount does not match what actually shows up

- “Gift” that is really a loan (repayment expected)

- Mixing gift funds with other deposits so the trail becomes unclear

- Assuming gifts can satisfy reserves (VA and USDA often do not allow this)

The smoothest closings happen when the gift documentation is handled early, with clean transfers and clean statements.

A Quick Playbook For Buyers

- Tell your loan advisor you plan to use gift funds during pre-approval

- Confirm the loan program’s donor rules (and whether any borrower contribution is required)

- Get the gift letter signed early

- Transfer funds using a trackable method (wire/ACH/cashier’s check)

- Save transfer confirmations and PDFs

- Avoid new large deposits that are not clearly documented

- If donating directly to title, coordinate early so the closing disclosure reflects receipt correctly

Bottom Line

Gift funds can be a great way to get into a home sooner, but they only work smoothly when they’re documented correctly. Every loan type has rules on who can gift, what the funds can be used for, and what paperwork is needed to prove the money is truly a gift and not an undisclosed loan.

If you’re planning to use gift funds, let’s talk early. We’ll confirm what your specific loan program allows, help you structure the transfer the right way, and tell you exactly what documents to collect so underwriting stays clean and your closing stays on track.

This blog post is intended for informational purposes only. It does not constitute financial advice, an offer to extend credit, or a commitment to lend. Mortgage rates, program guidelines, and qualification requirements can change at any time and may vary based on credit, income, assets, location, and property type. Always consult with a licensed mortgage broker to review your personal situation and available options.

Enjoyed this article?

Share it with your network